-

By Anil Trivedi

By Anil Trivedi

- May 3, 2026

- 0 Comments

- Tire Industry

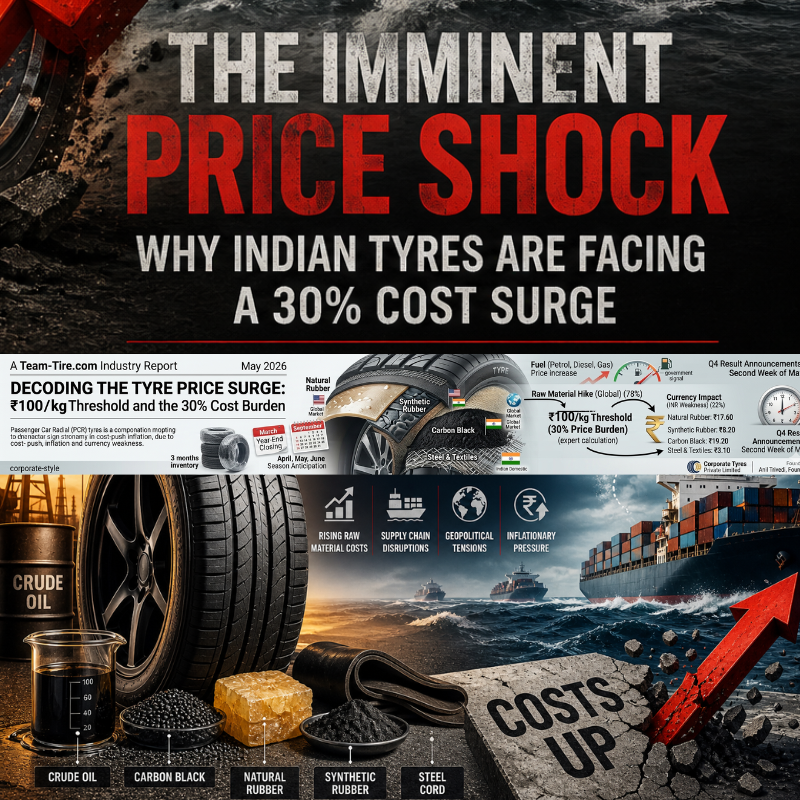

The Imminent Price Shock: Why Indian Tyres Are Facing a 30% Cost Surge

The Indian tyre industry serves as the literal foundation of a nation’s mobility, acting as the critical interface between vehicle and road. In a rapidly growing economy like India’s, tyres are more than just rubber and cord; they are a barometer for industrial health, logistics efficiency, and consumer sentiment.

For several quarters, manufacturers have acted as a shock absorber for the Indian economy, shielding consumers from a massive inflationary “cost-push” that has redefined the economics of production. However, as of May 2026, the industry has reached a breaking point where internal math simply no longer supports current retail pricing. The following report details the expert calculation behind the ₹100/kg threshold and the systemic reasons why a massive price correction is now inevitable.

The Expert Calculation: Decoding the ₹100/kg Threshold

According to the Team-Tire.com expert calculation, the cumulative impact of rising global raw material costs and currency depreciation has reached a staggering ₹100 per kg.

The 30% Cost Burden

For a standard Passenger Car Radial (PCR) or Truck and Bus Radial (TBR) tyre, this represents a massive 30% increase in production costs. If this were passed on entirely today, it would represent an unprecedented financial burden on the Indian consumer. To understand this ₹100 figure, we must break down the two primary economic forces at play:

The Global Commodity Surge (78% of the burden): Global prices for the “material basket”—including rubber and oil derivatives—contribute ₹78.00 to every ₹100 of cost-push.

The Currency “Tax” (22% of the burden): The weakening of the Indian Rupee (INR) against the USD adds an additional ₹22.00 to the cost. Because many tyre precursors are imported, a weaker Rupee makes every gram of material more expensive for Indian factories.

Breaking Down the ₹100 Impact Logic

The “₹100/kg hike” isn’t a single event but a combination of two powerful economic forces working in tandem:

The Global Commodity Surge (78% of the burden): Global prices for the “material basket”—including rubber and oil derivatives—contribute ₹78.00 to every ₹100 of cost-push.

The Currency “Tax” (22% of the burden): The weakening of the Indian Rupee (INR) against the USD adds an additional ₹22.00 to the cost. Because many tyre precursors are imported, a weaker Rupee makes every gram of material more expensive for Indian factories.

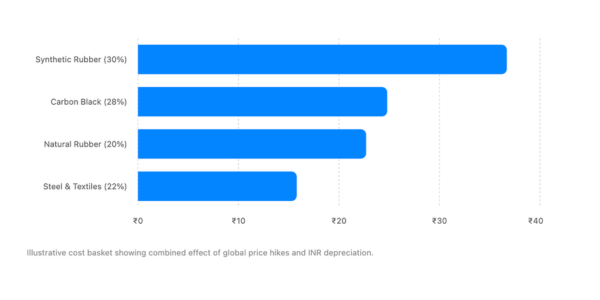

Component Sensitivity: Where the ₹100 Comes From

Based on industry technical analysis, the breakdown per ₹100 of impact is as follows:

1. Synthetic Rubber (30% Weight | ₹36.70 Impact)

Synthetic rubber is the largest single cost driver. Tied directly to the price of crude oil, its volatility is compounded by currency shifts. As global oil prices remain elevated, the cost of the butadiene and styrene needed for high-performance PCR tyres has reached historic highs.

2. Carbon Black (28% Weight | ₹24.80 Impact)

Carbon black provides tyres with their strength, abrasion resistance, and characteristic color. As an oil-based product, it has seen a dramatic rise in input costs, significantly impacting the “bleeding” of manufacturing margins.

3. Natural Rubber (20% Weight | ₹22.70 Impact)

Despite the rise of synthetics, natural rubber remains essential for the sidewalls and heat-resistance of truck tyres. Global supply volatility, driven by climate factors and labor shortages in Southeast Asia, has added nearly ₹23 to the per-kg cost-push.

4. Steel & Textiles (22% Weight | ₹15.80 Impact)

The radial structure of modern tyres depends on high-tensile steel cords and specialized textiles. While these are the most stable components, they still contribute significantly to the overall burden.

The Inventory Factor: Why the System is Overloaded

A key reason why this cost-push is becoming critical now is the way the industry manages its supply chain and seasonal cycles.

-

Year-End Stocking: The industry generally operates by building three months of inventory; as March marks the year-end closing, heavy stocks are pushed into the system as dealers work to complete their annual targets.

-

Seasonal Anticipation: In anticipation of the peak season months of April, May, and June, the tyre industry tends to start building additional inventory from March onwards.

-

The Price Lag: Because this massive volume of stock was manufactured or moved into the system during the year-end push, it carries the heavy burden of the ₹100/kg cost-push. Manufacturers are currently sitting on expensive inventory while waiting for the market to accept higher price points.

The OEM Benchmark

This disparity is stark when compared to vehicle manufacturers (OEMs). Truck and car manufacturers have already implemented price hikes of up to 6% to manage their own rising input costs. The tyre industry, by contrast, has stayed in a state of “margin sacrifice”.

Segmented Industry Trends: A Multi-Sector Inflationary Wave

The “bleeding” observed in the tyre sector is part of a broader inflationary trend across all automotive and industrial ancillary businesses. Since January 2026, similar sectors dependent on crude derivatives and global commodities have already initiated significant price corrections to survive the cost-push. The lubricant (mobil oil) industry has implemented surges of 8% to 15% as base oil prices track the post-election “unfreeze” in energy rates. Similarly, the paint industry has seen cumulative hikes of 8% to 12% since January, with market leaders announcing fresh 3% to 5% increases in early May 2026 to protect margins. Even the battery segment has passed on increases of 5% to 10% due to rising lead costs and currency-driven import expenses. These movements underscore that the tyre industry’s current 2% to 5% adjustments are vastly trailing the broader market reality.

The Gap: Why Have You Only Seen a 2–5% Increase in Tyres?

Despite the expert-calculated ₹100/kg (30%) cost-push, manufacturers have been conservative with their pricing across different segments:

-

Truck and Bus Radials: This segment contributes 60% to 70% of the industry’s total value, yet prices have only seen a modest increase of 2% to 5%.

-

Passenger Car Radials: The next largest segment by value has seen a mere 2% to 3% increase.

-

Two and Three-Wheelers: Despite being the highest volume segment, price increases have been limited to 3% to 5%.

Why the delay?

Much like the government held back petrol, diesel, and gas price hikes for the election cycle, the industry avoided “sticker shock” for consumers. Additionally, in an oligopoly, no one wants to be the first to implement a double-digit hike and lose customers to a competitor.

The Perfect Storm: Fuel and Financial Results

The pressure on the tyre industry does not exist in a vacuum. Manufacturers and consumers alike are now facing a secondary wave of inflation.

1. The Post-Election Fuel “Unfreeze”

Following the recent election cycle, the government has begun signaling imminent price increases for petrol, diesel, and gas. For months, fuel prices were held steady to maintain economic stability; however, the “unfreezing” of fuel rates will inevitably drive up freight and operational costs for tyre manufacturing.

2. Q4 Result Announcements: The Second Week of May

The industry is currently holding its breath for the final Q4 result announcements, expected to be completed by the second week of May 2026. These reports are expected to show significant “bleeding”—with profit margins compressed as companies paid high costs while only recovering a fraction from the market

Conclusion: Preparing for the Mid-May Correction

By the second week of May 2026, the financial reality of the industry will be public. The data suggests that manufacturers—from global leaders to specialized domestic firms—will likely have no choice but to initiate a significant price correction to stop the severe financial bleeding caused by the long-term absorption of costs.

The industry is currently transitioning from a period of strategic “wait and watch” to one of necessary survival. With the expert-calculated ₹100/kg impact (30% cost surge) now fully baked into the massive inventory built during the March year-end closing, the current price levels are no longer sustainable.

At Team-Tire.com, we remain committed to modernizing the Indian tyre market through technical excellence. However, sustainable growth requires a balance between engineering and economic reality. The ₹100/kg impact is real, and the coming weeks will determine how the industry navigates this 30% challenge.